What Trump’s New Tariffs Mean for Investments

Let’s cut through the noise.

You may have seen headlines about President Trump’s latest trade announcement and the impact it’s having on markets. While the news can feel unsettling, we want to help cut through the noise and explain what’s going on—and how it could affect your investments.

This update gives you the key facts, outlines what we’re watching closely, and explains how portfolios are positioned to navigate periods like this. Uncertainty is a natural part of investing, but rest assured, we’re focused on the long-term picture and helping you achieve your financial objectives.

What just happened?

President Trump has delivered his “Liberation Day” announcement, ending weeks of anticipation and speculation. The measures were toward the more extreme end of expectations. We will try not to repeat what is widely available in the press, but it’s worth a quick reminder on the background behind last night’s executive order.

Very early in his second term, President Trump ordered the US Trade Representative to investigate potential trade frictions imposed by America’s trading partners which might cause their exports to America to be more competitive than America’s exports to them. He asked for it to be a thorough review going beyond tariffs to also include non-tariff barriers.

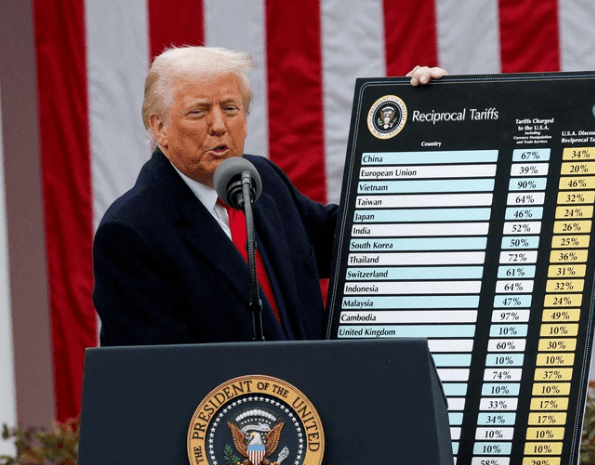

What was announced?

Despite decades of progress in reducing tariffs and trade barriers, there remain frictions and to some extent these are inevitable.

The impact of this is significant. The average tariff suffered by US imports has risen by around 20% so far during his second term. He has indicated further tariffs will come to cover pharmaceuticals, semiconductors, lumber, and copper.

At the end of March, this report was produced and, based upon it, the administration have determined that every country exerts protectionist policies which the US needs to reciprocate. That includes 115 countries with an identical implied tariff on US imports of 10% which will be fully reciprocated and 75 countries with implied tariff rates of greater than 10% which will be partially reciprocated with tariffs ranging from 10% to 50%

This comes after tariffs which President Trump introduced during his first term on China and metal imports. This year he has now raised tariffs on China three more times – reaching a cumulative rate of more than 60%. This includes tariffs related to fentanyl imports which also apply to Canada and Mexico. Sector specific tariffs of 25% have been announced on US imports of steel, aluminium, cars, and car parts.

How will this affect the economy?

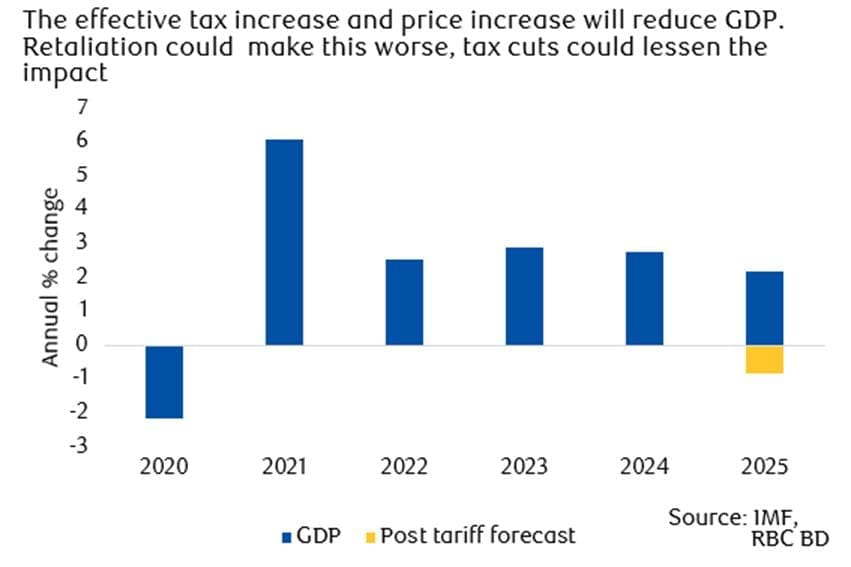

Best estimates of the impact on growth from these tariff measures is that they could reduce US GDP by around 3% while prices are likely to rise by more than 1.5% due to the measures. These figures are relatively easy to estimate as they reflect the increase in prices and taxes. The potential offset to this would be if the government were to return the tariff revenue to the economy through tax cuts. They almost certainly want to do so, but when the Congressional Budget Office forecasts the sustainability of tax cuts, we don’t believe they will be able to count this revenue because these tariffs have been imposed under emergency measures, not written into law. Nevertheless, we should assume some US tax cuts which will partially offset the pain of these measures.

Ordinarily we would expect currency appreciation from the country imposing a tariff (less dollars get exchanged for foreign currency to buy imports) but it is striking how the dollar has fallen sharply since it became clear President Trump would take on all countries simultaneously. This reflects the fact that US growth is expected to suffer more than the growth of US trading partners. The US will suffer an increase in taxes and prices relative to all of its trade. It will also face retaliatory measures from many countries (the Eurozone and China have already confirmed this). Trading partners will only suffer this in relation to their trade with the US.

The Federal Reserve will probably cut US interest rates this year, although with inflation potentially breaching 4% during 2025, it won’t be an easy decision, especially with the weak dollar. The ECB and MPC are quite likely to cut at their next meeting.

Will these policies be effective in reducing the US trade deficit?

To some extent they will, but historically the US trade deficit has contracted at times when the US economy slows, so it can seem like a victory at a very high cost. The reason America runs a trade deficit is because American consumers spend more than they save, something which is made possible by the Federal government paying out more in entitlements than it earns in tax revenue. These tariffs are substantial but still not enough for most emerging economies’ exports to be uncompetitive relative to US manufacturing. US productive capacity is insufficient to meet its domestic demand, and that situation will only worsen due to immigration curbs. Without immigration, America’s work age population is due to start declining. Therefore, it seems unlikely that these policies will spark the manufacturing revolution President Trump is trying to achieve.

What happens next?

Above all the two key truths about Donald Trump remain as relevant now as ever:

- He has a fetish for tariffs (which he is currently indulging).

- He loves to negotiate.

There is no question that the impact of these tariffs is negative for the global economy. There are environmental and social consequences of trade, but it is economically positive, and its curtailment is a headwind. He has already signalled his willingness to negotiate and the unpopularity of prices increases should encourage him to come to the table, so it would not be surprising to see these tariff rates reducing over time in a succession of triumphant announcements.

There is no question that the impact of these tariffs is negative for the global economy. There are environmental and social consequences of trade, but it is economically positive, and its curtailment is a headwind. He has already signalled his willingness to negotiate and the unpopularity of prices increases should encourage him to come to the table, so it would not be surprising to see these tariff rates reducing over time in a succession of triumphant announcements.

How will this impact investments?

Markets have been bracing for this announcement for weeks. Now that it has landed it was towards the more extreme end of what investors considered possible and that has weighed on the markets since they have reopened. The impact on companies is complex and varies stock by stock. The impact does not depend upon where companies’ shares are listed, or even where they sell their goods, but rather where they manufacture their goods.

After two years of strong stock market returns a period of volatility reminds us why it is useful to include defensive assets within portfolios. Gold has given good protection although it is suffering from profit taking as we write this. This probably reflects some investors’ view that we are approaching or passing the position of maximum uncertainty. Different types of bonds respond in different ways to changes in the economy. For example, government bonds often hold up better during periods of slower growth, while corporate bonds can be more vulnerable. That’s why we believe in staying diversified—spreading investments across a range of bond types helps manage risk and smooth out returns over time.

These periods of volatility are stressful, but they also offer opportunities, so we continue to be vigilant in our assessment of the big picture as well as individual investments. As always, we are monitoring portfolios and we are here to answer your questions. Please contact us with any questions.